WEALTH UPDATE - 3rd Quarter 2020

The era of dislocation is upon us.

Never before have we witnessed such a wide dispersion on so many levels as we have experienced thus far during 2020. From the exuberance of investors in US technology stocks to the despair of investors in South African property and financial shares. From US unemployment being at its lowest level in history to more than 40 million people losing their jobs in the US 3 months later…

One common theme does however prevail, no matter where you are situated in the world you would have been impacted by Cocid-19 either financially, socially or health wise. What we also must brace ourselves for is that the economic and social turmoil is not over yet, and no one can say with certainty when normality will return globally and what that normal will look like.

“Therefore, it’s not a question of announcing a date for return and saying everything is done. Instead it’s about a process, one that will have a series of ups and downs. In fact, two steps forward and one or more back, may be the story of our times. We need to be able to live with disruption as usual and respond with a tailored, relevant set of actions ”

With turmoil comes concern, negativity, and despair. Unfortunately, in South Africa we did not need a foreign virus to add to our woes, we have buckets full of our own problems even without Covid-19. South Africans’ confidence levels are at a low with Government debt spiralling out of control, corruption rife and load shedding still part of our lives. The fact that South Africa is seen as the black sheep (am I allowed to say that?) of the family by many and sentiment worsened by very disappointing investment returns over the past 6 years make many want to pack their bags and become sheep farmers across the big pond.

As an eternal optimist I thought that I have to find some glimmering lights of hope to give investors and South Africans in general, the hope to hang in there because things are not as bad as they seem. Before your party hats go flying again, I must state that things are pretty dismal, but they could have been much worse…Dr Dlamini Zuma could have been president…

I first thought that I was going to bombard you with facts and figures but found that impossible since data changes multiple times a day not even to speak about monthly and quarterly. By the time you would have read this newsletter the information would have changed so radically that I would have looked like a fool!

To bring some perspective to our woes I gathered information about some of the most topical issues that surround and concern us as South Africans. In this newsletter I am going to try and put a positive spin on the following:

Eskom and load shedding. Is that light at the end of the tunnel Eskom powered or is it a train approaching?

South Africa’s debt trap. What must happen to prevent the debt trap and prevent SA from falling off a cliff.

Our frail and worsening economy. How are we ever going to achieve economic growth if most of the funds raised by Government goes towards the governments wage bill and servicing debt?

Corruption and the fight against it.

The weakening Rand. Is this a rand-zipline on its way to Zim dollar status?

Where to from here?

The bottom line is we (SA) needs to make sufficient changes to boost investor confidence and attract new local and foreign investment into our economy. That is the only way to reduce unemployment and place SA on a growth trajectory which should be closer to 5% per year than sub 1% per year.

Unfortunately, Covid-19 magnified and multiplied the above problems. Before Covid-19 SA was already in a recession with huge challenges facing us. Today the situation is dire with unemployment at 42% and our budget deficit worse than ever. Urgent action needs to be taken to prevent a catastrophe. However, Covid-19 which created so many problems may also at the same time have created an opportunity to fast track the fixing of the above-mentioned concerns.

Eskom

Without sufficient reliable power supply business cannot operate and we will not receive new investments into our country leading to a stagnant dying economy pretty much like we are currently experiencing.

My mood was lifted recently after attending a webinar with Andre de Ruyter (CEO of Eskom) and my optimism received another boost after another webinar where Duncan Pieterse (Head of Economic Policy at the National Treasury) was a guest. The 2 webinars were unrelated, but I was encouraged by the similarity in the messages that came across. In summary the following was conveyed:

What has changed from April this year (in previous correspondence I eluded to developments from January to March)

Debt has grown to R 488 billion (this is a negative aspect). However, several governments, international development institutions and banks are willing to replace current Eskom debt with cheaper “green money” on condition that Eskom transitions from coal-fired power stations to cleaner energy that will reduce emissions.

Eskom is committed to follow this path as laid out in the IRP (South Africa’s Integrated Resource Plan) which was approved in 2019. It is envisaged that 11 000 MW of coal-fired power stations will be decommissioned by 2030 and some 24 000 MW more after 2030.

De Ruyter’s vision is that existing Eskom power plants can be refurbished as gas-fired stations and land adjacent to power stations can be used for solar energy. Mpumalanga has more sunshine than Germany where solar power forms a large part of power generation.

Eskom may form joint ventures with private companies by putting the power stations and adjacent land into JV’s as a capital contribution with private sector providing cash to refit stations for gas or renewable plants.

The way out of debt is greener power. A target date for debt restructuring is the next global climate change conference in Glasgow in November 2021.

Load-shedding is determined by 3 things: maintenance, Medupi and Kusile coming online, and new generating capacity. “Deep maintenance” should be completed by March 2022. Until then load-shedding will be with us. The cooling towers of Medupi and Kusile need to be lengthened by 12 meters to enable full capacity. This takes 75 days per tower and the current completion dates are 2021 for Medupi and 2023 for Kusile. Until then these 2 troubled power stations will operate at reduced capacity.

The most dramatic change since March concerns new capacity. The green light has been given for 14 000 MW of new capacity to be installed by 2024. This is significant considering that Eskom can currently produce around 30 000 MW on a good day. Most of it will be procured from independent producers – a big boost for investment and private sector involvement in power generation. The first phase of the power consisting of some 2 000 MW “emergency power” must be available by no later than June 2022. This expansion will be by way of gas-powered power stations and gas is 50% cleaner than coal.

The real boost to capacity comes from round 2 where construction to produce an additional 11 800 MW will probably start in 2022 with energy flow starting by mid-2023.

The 2 000 MW emergency power is expected to generate investment of R 80 billion by June 2022. The investment impact of the additional 11 800 MW will be clearer as the auctions for the construction proceed but it is useful to remember that 6 000 MW renewables since 2011 has generated more than R 200 billion in investment.

It is envisaged that after 2030 more coal-fired capacity will be closed and more new capacity will be built. Apart from greener power, these plans support industrialisation and will dramatically expand the gas industry.

The anticipated unbundling of the 3 business units of Eskom will open the door to competition in generation and distribution, drive transparency in prices, squeeze inefficiencies out of the system and pave the way to private investment in both generation and distribution.

Energy may well be the new investment frontier in South Africa.

Prior to Covid-19 privatisation of any asset of Eskom was contested aggressively by unions and related parties. That resistance has subsided and hardly attracts a reaction if mentioned today…

The pending debt trap.

The graph below is clear. If nothing is done and the current scenario persists (the passive scenario), then defaults on our sovereign bonds is almost unavoidable and SA will fall off the debt cliff.

Fortunately, there is a solution provided government acts prudently and with urgency leading to the active scenario shown in the graph. If this route is followed, SA can flourish. The challenge is huge, but doable. In the current scenario it will become clear if President Ramaphosa and his merry men are prepared to do what is right for the country or if they will persist and do what favour’s the ANC and attract voters….

What is the reason for debt to have spiralled in the manner it has done and projected to carry on doing so if nothing is done to change the trajectory?

Just like with a personal budget where one has one of 2 choices to improve your cashflow, government has the same predicament. So, what is the solution?

Increase your income, or

Reduce your expenditure

This sounds very simple if you say it quickly. Government’s problem to increase income is a real challenge. Government’s income mainly consists of taxes and levies raised upon businesses and individuals. Considering the current dire economic environment where our GDP is frailing and taxes on business and individuals is at a realistic peak, then government is forced to look at alternative income sources. The term “prescribed assets” on pension funds gets flung around loosely often causing concerns for many South Africans.

At this point government has taken prescribed assets off the table. Industry (fund managers, business in general and financial institutions) have suggested alternative options to prescribed assets. In short these options involve “herding funds” within investment funds where they can be applied to invest in financially viable projects like energy (my comments under Eskom), rail, transport, telecommunications, infrastructure etc. thereby getting private industry to not only fund these projects but to also obtain part ownership in them and create employment which we desperately need to do. This was confirmed in the webinar by Duncan Pieterse who I eluded to earlier. Treasury and government (some government officials are opposed to it for obvious reasons…) are in full support of this initiative. Should this initiative not be successful then I believe prescribed assets will become topical again.

Government expenses

The continues bailing out of SOE’s has added to government’s debt woes. Over the past 10 years SA added more debt relative to GDP than any top 20 Emerging Market country except Argentina…

I see this as the biggest challenge that government faces today. Considering that 51% of our national budget goes towards the government employees wage bill (the biggest wage bill as a % to GDP in the world!) it is obvious where the biggest cuts to expenses can and must be made. Herein lies the challenge. These government employees are also voters and they earn substantially more than their counterparts in private industry. Tito Mboweni spelt out the importance of cutting the wage bill and Cyril Ramaphosa endorsed that. This week COSATU and other unions are taking to the streets to fight for government wage increases after Cyril announced a restriction to wage increases. This battle between government (ANC) and its major ally (COSATU) is far from over and is bound to become heated. It is however encouraging to see that it seems as if Cyril has drawn the line in the ground on many fronts. This will not make him popular but that is what SA needs.

The second largest government expense is the servicing of debt at 20% + of budget. This will be more difficult to get right than the wage bill especially after the sovereign downgrade we received in March.

By allocating more than 70% of the annual budget to wages and servicing debt there just simply are no funds left to spend on the things that matter most like education, health and infrastructure. Once again, much to the despair of many government officials, there is no choice but to invite private sector into this space which was always closely guarded by government.

The easiest way to encourage economic growth and recovery is to accelerate the expansion and maintenance of infrastructure. That will reduce unemployment drastically, increase revenue and kickstart consumerism - everything that is needed in an emerging market like South Africa. Government will however have to re-allocate funds from the wage bill to infrastructure spending. It does seem like government has the same view as confirmed and acknowledged by Duncan Pieterse during the webinar. Let’s hope…

Corruption

On many occasions in the past I referred to the pace (or lack thereof) of prosecutions and the fight against corruption. President Ramaphosa is a strategist and I believe that he had to maintain his “independence” as far as pointing out corrupt parties is concerned. It took a major effort to re-build the NPA (assisted by the Asset Forfeiture Unit) to be a reputable organisation once again. The same applies to SARS and the Hawks.

Now that these units are functional, we can see the wheels of justice coming in motion. It was a major move forward when the President signed into law that evidence obtained by The Zondo Commission can be used as evidence to charge implicated parties for corruption. Ever since this became possible the arrests of prominent businesspeople, politicians, ex-politicians, senior members of municipalities and government officials and their spouses has accelerated with news of arrests literally breaking daily. The Asset Forfeiture Unit has been active seizing luxury vehicle, property and bank accounts of implicated individuals and companies. It seems like at long last justice is now being served.

Let’s see what the investigations into the Estina Dairy Farm debacle in the Free State delivers. We may just see the most prominent political person to date being charged soon. It’s interesting to see the pushback from some senior ANC officials against the investigations of their cadres and against the rule that Cyril made that government employees’ spouses and family will in future be prohibited to obtain government contracts as service providers.

It is also enlightening to see how corrupt parties within various organisations and SOE’s are being brought to book. This applies to current and past executives and people of influence.

We must however accept that the cancer of corruption is so deeply entrenched within the system that it is like trying to fight a fire while a bunch of arsonists are running around with blow torches in a windstorm. This became evident once again during Covid-19 where corruption thrived from food parcels being sold to dodgy contracts being awarded to plain theft. This is hugely frustrating but an unfortunate trait of the community we find ourselves in. What is important though is that action is being taken and parties are being held accountable for these criminal acts.

Perhaps a new fund that invests only in prison buildings and supplies is not a bad idea?

The Weakening Rand

We entered 2020 with the Rand at R 13,88 to the USD. During March we suffered a double whammy with a downgrade on our sovereign debt as well as Covid-19 resulting in the Rand to weaken to its weakest level ever at close to R 19,20 to the USD for a brief moment whereafter it started a recovery as can be seen in the graph (no.1) below. The graph below shows the Rand vs USD movement over the last year.

In the past we have had the Rand blowing out on several occasions most notably (see graph no.2 below which shows the 25 year pattern of the Rand vs USD) being in January 2002, January 2009, January 2016 and now again in March 2020. The graph below shows that following each of these periods of severe weakness a period of recovery followed after which normalised depreciation took place. Taking the above dates into consideration, then it took investors who took their funds offshore during these periods of weakness, 13 years to get to the 2002 level, 5 years to get to the 2009 level, and 4 years to get to the 2016 level. Who knows how long it will take to reach the R 19,20 level again.

As South Africans we tend to get extremely pessimistic when the Rand depreciates, and we often hear comments that we are heading to Zim Dollar status. It is a fact that the Rand will continue to depreciate like any emerging market (and many developed markets). If we look at the 25-year graph, then the Rand was at approximately R 3,70 to the USD 25 years ago. Now it is at a dismal R 16,60. Right? If we annualise the depreciation then R 3,70 to R 16,60 equates to an annualised depreciation of 6,2% per year and that is not bad at all. Unless SA defaults on debt repayments and we don’t do silly things like Turkey did (which by the way was the main cause why the Rand depreciated unexpectedly again in August this year (see graph 1) then there is no reason why we should expect the Rand to keep on depreciating at around 6% per year going forward. Unfortunately, depreciation does not take place in a straight line as can be seen in both the short term as well as long term graphs.

To put the Rand depreciation into perspective, have a look at the graph below which indicates the level of depreciation experienced by various countries over various periods. Although the Rand depreciated more than the developed markets, its depreciation rate is spot on and better than the average emerging markets currency

I have mentioned before that the rand is one of the most liquid currencies in the world and most certainly the most liquid emerging market currency. Global investors often use the rand as a proxy for emerging markets which leads to heightened levels of volatility as they move into and out of the “emerging market”. When Turkey tightened their money supply in August freezing up liquidity of the Lira, global investors sold Rands to reduce their emerging market exposure. These erratic moves often leads to swings between being the worst performing currency to the best performing currency in the world like it once again did this year.

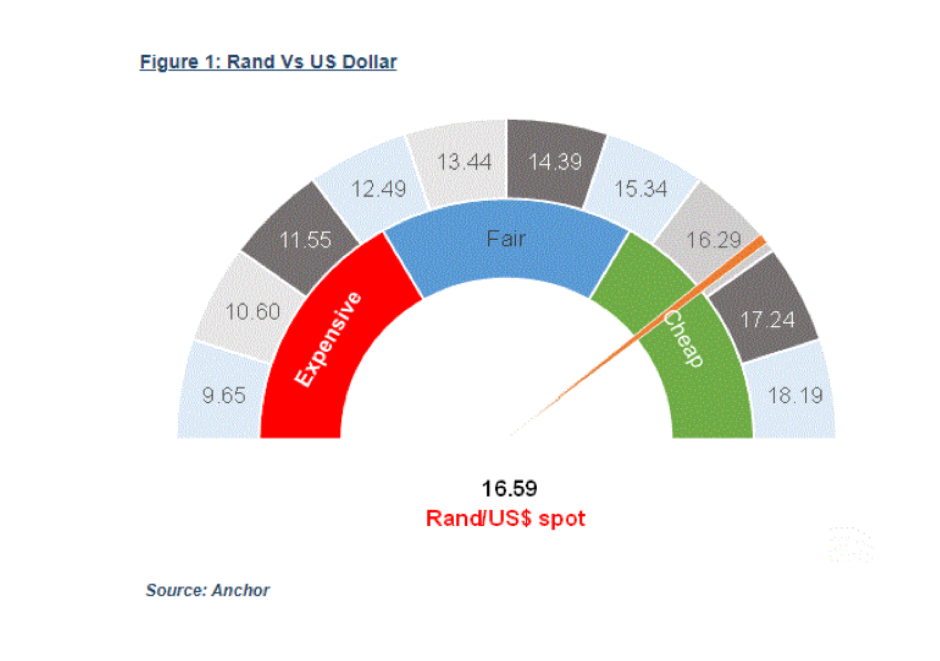

Where do we see the Rand Go? No idea in the short term! The Rand dashboard below is some kind of indication how some managers see the valuation of the Rand.

According to the “currency rev counter” the Rand has room to strengthen to fair value of somewhere between R 14.00 and R 15.00. I think this will be a challenge but possible. However, much of the concerns mentioned earlier in this newsletter around Eskom, corruption, unemployment and most importantly debt will have to be addressed for this to happen, But…nothing is impossible!

Where to from here?

In my opening comments I referred to the level of dispersion and dislocation across various fronts. Opinions on market returns and expected market recovery and the shape thereof vary as much as market returns have done so far this year.

Comments are made in the press of how one should have invested in the S&P 500 and how well the US economy has done compared to SA and how one should continue to invest in the US going forward and avoid SA at all costs. SA returns are branded as being dismal. This newsletter has already grown longer than I anticipated so I am not going to delve into this subject in detail. All that I want to state is that apart from the US market, and the Nasdaq in particular, all markets have performed poorly for a very long time now.

In the US the big 5 Tech stocks (FAANG) have pulled up the market exponentially. Remove these 5 shares form the S&P 500 and the US market is negative for the year by a similar % as the SA market. See graph below.

Even though we believe that these tech companies (FAANG) are structurally strong and that they are totally different animals to the ones that led to the spectacular tech bubble and implosion of the tech industry in early 2000, they are priced for perfection. It is widely expected for them to continue their upward trajectory and it is common to hear expected returns of more than 25% per year. To put this into perspective consider the following: Currently FAANG make up approximately 22% of the US market. If they grow at 15% per year and the other US shares carry on their current trajectory, then in 5 years’ time FAANG will represent 87% of the US market. If FAANG grow at 25% per year as widely speculated, then in 5 years’ time they will represent 127% of the US market. That is a tall order, even for FAANG.

Investing is about buying decent assets at a good price. It is unknown how long it is going to take for Covid-19 to leave us in peace and for the world to start building its economy again. During this pandemic, some markets suffered more than others. During times of crisis world investors flee to safety which generally means away from emerging markets. This time was no different. Emerging market shares are currently trading at a discount of more than 30% compared to developed markets. At the same time these companies have half the debt to equity making them very appealing.

See graphs below.

My comments above do not imply that all your money must now be invested into emerging markets. I am merely trying to point out that there are solid alternatives to US tech stocks, which you must own by the way (just don’t bet the house on only FAANG). It all comes back to diversification and a well-constructed portfolio if you want to earn decent returns over an extended period.

We don’t know:

When Covid-19 is going to be beaten

When world markets are going to be fully recovered

What the impact is going to be if Biden or Trump wins the US election

How long interest rates are going to remain at negative real rates worldwide although the Fed has indicated at least 3 years

What the “new normal” is going to look like

We do know:

Cash at the moment is not a good investment considering the low and no returns offered.

Global bonds are just as bad as (if not worse) than cash. Here SA is the outlier offering the best bond yields in the world (but be careful, bonds are priced cheap for a reason…)

Property is structurally weak and will possibly face more headwinds. Long term potential returns look promising at these levels but be prepared to take more losses before gains come through

Equities are the only logical asset class that can provide real returns into the foreseeable future. This does not mean that you should apply all your assets to equities. It does however mean that you may have to increase your exposure to equities slightly and accept more volatility for some time to come

In short, equities over cash. Offshore over SA. But do not turn your back on SA equities completely. They are known to come back and surprise on the upside when no one expects it...

If anyone is interested to listen to the interview with Duncan Pieterse please contact me for the website details where to find it.

Unfortunately we have been requested not to distribute the interview with Andre de Ruyter since some sensitive issues and facts were discussed.

Stay safe and stay invested and most of all, thank you for your continued support.